This year, the outlook for critical minerals mining and processing projects has dramatically changed. For a decade, critical mineral projects have struggled to get access to capital, despite surging demand and a political desire for critical mineral independence in many developed economies. Under mounting pressure from China's dominance in critical minerals, those policy ambitions have now shifted from strategic intent to a new capital architecture that actually accelerates capital deployment across mining, processing, refining, and related infrastructure. However, although more capital is now available at scale, that access is increasingly selective. Only critical mineral mining and processing projects that have environmental and social performance deeply embedded in their design will benefit.

Building momentum for coordinated action

The supply chain disruptions of 2020-21 and the energy security shock of 2022 triggered the first wake-up call for developed economies, revealing how much their economic resilience depends on secure access to raw and processed minerals and the dangers of relying on a handful of suppliers, particularly China. European, American, and Asian governments started talking about the need for independence in critical minerals, both in mining and processing, and to support the sputtering supply chain outside China by improving access to capital.

However, it took the profound trade and geopolitical shocks over the last few years, combined with China's accelerating dominance in critical minerals, to translate the political conversation into action. The competitive context is stark. Since 2023, China has deployed more than USD 340 billion in vertically integrated critical-minerals investments: USD 120 billion in overseas mining and upstream refining of raw ores, and USD 220 billion in transforming refined materials into high-value components in batteries, EVs, grids, and solar panels.

As a result of multi-year investments, China currently controls approximately 90% of rare earth refining, 70% of cobalt refining, and 60% of lithium processing. China also isn’t afraid to use its supply chain leverage when geopolitical tensions flare. Chinese shipments of rare earth magnets, crucial for electric cars, wind turbines, and missiles, to the US fell by 22.5% year on year in the first two months of 2026, while global exports rose by 8.2%.

On top of the push for critical-mineral independence in developed economies outside China, the products of the mining and metals sector are also hard to substitute, which adds to its momentum. A copper deposit or a separation facility cannot be disrupted by software or replicated in eighteen months. For pension funds and infrastructure private equity companies seeking inflation-linked, long-duration cash flows, this physical irreplaceability is precisely what they are looking for in this tumultuous era. Mining, processing, and the connecting infrastructure are what capital markets in 2026 call HALO investments — Heavy Assets, Low Obsolescence. This category of investors sees adherence to environmental, social, and governance (ESG) criteria as critical to maintaining stable returns and cash flow.

Ready to take on the twin deficit

Politicians in developed economies are now keenly aware of the urgency to tackle the twin issues at the heart of the critical minerals security completion: mining and processing. Even where new critical mineral mines can be developed within acceptable timelines, the raw ore must pass through refining and conversion infrastructure before it becomes a usable industrial input, and China controls the majority of that infrastructure globally. So, to achieve critical minerals independence, developed economies must expand both mining and processing.

Numerous Western and other countries have moved aggressively to do just that and boost critical mineral supply chains outside China, with the United States taking the lead. The Trump administration, for example, invoked national security powers to negotiate price floors for raw and refined minerals in order to shield domestic and allied producers from price volatility and predatory pricing. Another US initiative is Project Vault, a USD 10 billion Export-Import Bank (EXIM)-backed strategic critical-minerals reserve, to protect domestic manufacturers from supply shocks and support US production and refining of critical minerals.

The US also hosted a critical minerals conference for 54 nations, representing two-thirds of the global economy, which led to the creation of the Forum on Resource Geostrategic Engagement (FORGE), a framework for international coordination to integrate allied critical-mineral supply chains and stabilize markets. In the past six months, the US unlocked USD 30 billion for critical mineral projects through bilateral agreements, investments, loans, and policy coordination. In March, Canada announced USD 12.1 billion in partnerships with 12 nations using a similar approach, as well as a USD 3.5 billion investment to support domestic projects.

Spurred by these policy signals, major deals followed quickly. Glencore signed a USD 9 billion agreement to shift its copper and cobalt assets in the Democratic Republic of the Congo (DRC) into Western supply chains, with backing from the US Development Finance Corporation (DFC). Brazil's Serra Verde secured USD 565 million in DFC financing for rare earth production, with a US equity option, while unwinding its Chinese offtake agreements by end-2026. Infrastructure is also being locked in: the DFC committed USD 553 million to the Lobito Atlantic Railway linking the DRC and Zambia's Copper Belt to Atlantic ports, with the European Union adding over €2.2 billion to the same corridor through its Global Gateway initiative.

At a pace that has surprised even insiders, a new capital architecture has emerged, weaving together state capital commitments, market protections, policy support, and bilateral and multilateral coordination to structurally accelerate capital investments in critical mineral supply chains outside China.

However, this new capital architecture includes a non-negotiable prerequisite: only projects that have high social and environmental performance embedded throughout their lifecycle will gain access to the capital it can unlock.

The mining sector’s steady shift to lifecycle governance

|

For most of the industry’s history, the formal instruments through which mining companies reported on environmental and social performance were designed for discrete moments in the project lifecycle, such as exploration, construction, production, and closure. Reporting efforts for each moment were rigorous within their framework. Still, none were designed as a continuous governance system capable of ensuring and demonstrating positive performance throughout the entire project lifecycle.

Evidence of the damage caused by this lack of attention has been quietly accumulating. A few examples: the Fundão tailings dam failure in 2015 destroyed social license and cost more than USD 31 billion in remediation obligations; Pebble Mine’s failure to establish community and nature foundations destroyed years of equity investment without producing an ounce of copper; the inability of the Kallak iron ore project to manage biodiversity and Indigenous rights from the outset has cost nearly two decades of value.

Leading mining and metals operators understood this limitation long before their investors did. To avoid the fate of the examples above, they built internal environmental and social management systems and engagement frameworks. They made voluntary commitments that went well beyond what capital markets required or rewarded. The emerging Consolidated Mining Standard Initiative reflects how industry leaders have been building a solid social and environmental approach for years, which is now consolidating into a form that capital markets can verify.

The architecture of accountability has caught up with what leading mining operators have already recognized: regulators, politicians, and investors are now scrutinizing and enforcing social and environmental performance. The old model is structurally over. A proactive, holistic approach to social and environmental performance throughout the project life cycle is now paramount for gaining access to capital and avoiding debilitating delays or cancellations.

|

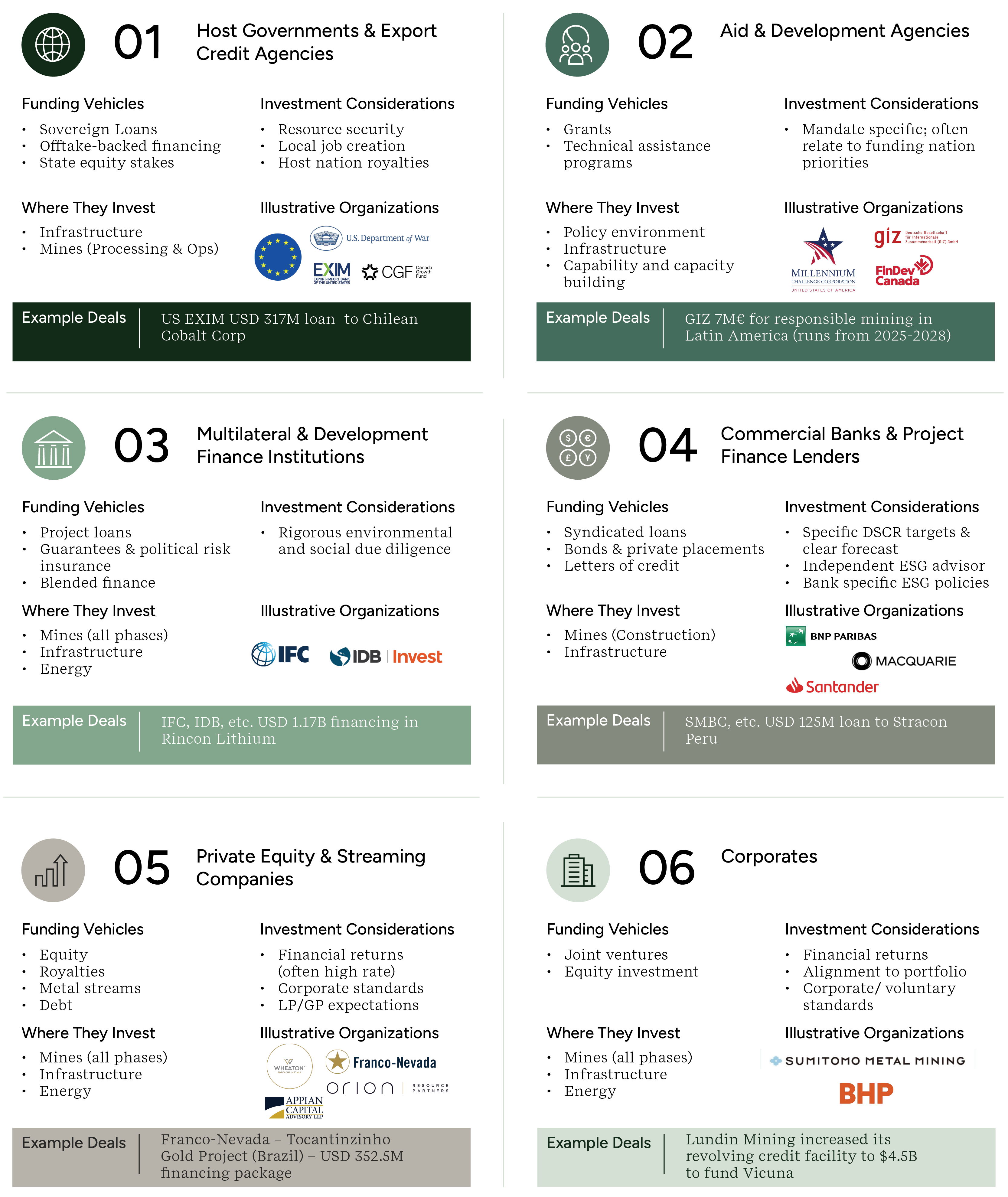

The new capital architecture: six pools, one ESG gateway

The new structure is roughly divided into six distinct capital pools, each with different instruments, return requirements, and most importantly, strict ESG standards. These six distinct pools are government financing agencies, multilateral development banks (MDBs), specialist private equity, pension funds, infrastructure investors, and original equipment manufacturers (OEMs). Each capital pool has its own set of criteria. However, all share the same gatekeepers — high expectations for environmental and community performance — which affect access to every layer of capital.

Six investor instruments to unlock critical minerals projects

A few illustrations on the pivotal role of ESG performance to get a foot in the capital door. For an equity investment by the US development finance corporation (DFC), a project needs to align with the rigorous IFC Performance Standards and be continuously monitored. Offtake agreements with automotive OEMs often include Copper Mark certification as a contractual obligation, while most pension funds acting as limited partners (LP) require quarterly portfolio-level ESG data.

The US or Canadian government will not extend a price floor or alliance guarantee if a project cannot demonstrate social license, environmental compliance, and rights-holder consent. Lastly, private equity specialists hardwire strict ESG criteria into every term sheet before a project is selected.

All six capital pools include strict requirements for water stewardship, rights-holder and stakeholder engagement, and nature impacts. High performance in these areas is crucial to the success of critical minerals projects. ERM’s

Mission Critical research, covering 226 major projects and 50 senior industry leaders, found that two-thirds of the projects experienced months to years-long delays, caused by permitting (45%), stakeholder opposition (26%), and environmental challenges (24%).

Mining companies that have already made serious efforts to embed sustainability performance at every stage are obviously at an advantage to benefit from the new capital architecture. For mining companies that still struggle to meet ESG requirements, potential access should be an additional incentive to invest in their social and environmental performance to avoid eroding their competitive position.

What next for mining and metals companies?

So, what should mining and metals companies do to tap into this new capital architecture? It will likely require calculated effort, since its participants have moved the goalposts on ESG performance. Below are three crucial steps many companies should take to prepare:

Analyze what makes the new capital architecture tick

- Every board and sustainability function needs to gain a thorough understanding of the potential sources of capital and the requirements to access it. Many capital providers set a high bar for climate, nature, and social performance prior to financing. Expectations go far beyond compliance, a community meeting, or building a local school. The yardstick is not meeting gateway conditions. It is whether a company has the organization, systems, and operational discipline that make meeting them a natural consequence of how the business is run.

Assess your company’s readiness for relentless live auditing of ESG performance

- With this new bar in mind, companies need to assess the gap between the information that their current disclosure instruments and management systems can deliver, and the live evidence stream that the participants in the new architecture, such as MDBs, national development finance corporations, and pension fund LPs, expect. The current situation may satisfy certain disclosure standards, but the new architecture no longer relies on annual disclosures; it is continuously auditing the system behind them.

Build a foundation that makes a lifecycle approach to ESG performance possible

- Before any baseline study, companies must first lay the general foundation needed to meet or exceed the new bar. It will take a robust approach to relationships with rights holders, water stewardship, nature management, and governance, all spanning the full lifecycle of the operation. On top of that foundation, the project asset can be carried through permitting, financing, construction, operation, and eventually its closure and next-use transition. The institutional memory of the asset’s location and of the people and ecosystems that share it must be stewarded through those transitions.

Companies that have already taken these steps will discover that the new capital architecture vindicates the decisions they made years before the market demanded them. The distinction between disclosure and performance — and which companies are ready for the latter — will shape the next cycle of capital flowing into mining and metals, as well as the ability of developed economies outside China to respond to Chinese supply chain dominance.